")

“You have to spend money to make money.”

This old adage is still a basic tenet of business today, but it’s especially relevant for modern real estate agents — and certainly, for those whose goal is to increase their revenue substantially.

There are several actions agents young and old, new and experienced can take to not only increase their earning potential, but also save more money in the process — including the expert financial best practices below.

Apply the long-term, money-making philosophy outlined below to get your agency on its way to a better bottom line from one month to the next (and get even more financial insights in this exclusive Placester webinar featuring top-producing real estate agent Jesse Garcia).

![]()

Select dynamic real estate technology that will increase your productivity and save you time.

We’re in the midst of the Digital Age of Real Estate. Therefore, it’s essential to know which tools will both save and earn you the most time and money — in other words, ones that help you attract, capture, and manage leads with relative ease and don’t take up much of your daily and weekly business calendar.

It can be downright overwhelming to wade through all of the available real estate tech apps and solutions out there, which, in turn, can make it tricky to decide which are the best fit for your agency. Having said that, there is a process you can use to gradually narrow your options so you can secure the most appropriate tools sooner than later.

Assess the tried-and-true real estate tech you already use.

Even if you believe learning to use technology is an uphill battle, you almost certainly already depend on several different apps and systems to enhance your day-to-day operations. Do you prefer to consistently update and use your real estate website to engage with your prospects? Or maybe you have a particularly robust CRM that’s essential to your client organization and lead nurturing?

Take stock of the tools you’re currently using to generate more business and notice the ways in which they are and aren’t serving you. For instance, maybe you want to dive headfirst into using ad retargeting on your site, but you aren’t using the Facebook Pixel, or maybe you already have a solid video marketing strategy and you’re interested in learning more about virtual reality tours.

Analyze if your current tools help you easily track leads and deals.

Whether you work as part of a team or fly solo, you’re hopefully always setting and working towards goals. The beauty and simplicity of using the proper technology is that those tools will enhance your productivity and help you achieve what you aspire to more quickly.

Do you measure success in number of houses sold annually? How many referrals-turned-clients you receive per month? Creating X number of new website content pieces in a week?

Whatever your goals are, your technology should assist you in carrying out these objectives by keeping you organized and able to keep in consistent contact with your prospects.

Determine if your agency website offers the best user experience.

As with everything about your real estate business, the customer perspective and experience should be your main priority. For instance, is your website difficult to navigate? If your leads are confused or annoyed when they first visit your site, or they can’t easily find what they’re looking for, you must put your energy into creating a more user-friendly site.

Like it or not, your website is often the first and only impression prospects have of your business, and if their experience is poor, they’ll look elsewhere for agent representation, causing you to lose money over time.

Plus, your prospective clients are using technology to search for, and interact with, available listings. That means if you’re struggling with necessary marketing tasks like producing the right types of content for your audience, or properly integrating your leads from various places into one CRM system, prioritize learning and developing your tech skills so you can provide your prospects with the most useful information possible.

Analyze past earnings trends to predict the future successes and stumbles your real estate business may encounter.

Just as past behavior is a a fairly good indicator of future behavior, the same rings true for how much your business can reasonably project in earnings over the course of a year.

Unless you decide to markedly increase your efforts to broaden the scope of your audience, or consistently test and implement new ways to increase lead engagement, the amount of revenue your business sees is likely to stay the same.

No matter your ultimate sales goals, you need to ensure they align with your marketing efforts and how much your actual income is.

The video below from The Real Estate Trainer explains the basics of drawing up a comprehensive plan for your real estate business by beginning with a primary goal and breaking it down into actionable pieces:

When you want to determine how your business will scale over time as you add more team members, or if you decide to expand your market size to include new neighborhoods and districts, it pays to begin tracking your sales records and income early on.

Why? For one, you’ll get in the habit of familiarizing yourself with how much money you have to work with to accommodate planned and unexpected changes in your business, and two you’ll begin to notice trends around the months you’re in the red, versus the occasions you nail a transaction.

To get in the habit of reviewing the nitty-gritty details of your finances every month, you should do several things:

- Make the most of your transaction management software to learn the specifics of your closed transactions and pending deals.

- Ensure whichever tools you choose have dual mobile and laptop functionality to keep your sales details in one place.

- If possible, select a system that allows for document uploading and synching so all information related to the sale can be easily accessed and referred to.

- Pay special attention to the trends in outgoing and incoming money to understand which areas you can change and improve your financial situation.

Evaluate all expenses for your real estate business, and develop a budget to minimize unnecessary spending.

No matter how long you’ve been working at growing your real estate business, proper money management is a must. If the idea of creating and sticking to a budget makes you scoff, think of the possibilities. It seems backward, but following a thoughtful budget can actually increase your cashflow in the short and long term.

Aspiring to up your earning potential when you are managing variable income each month will require careful planning and consideration of your resources:

Take note of all of your one-off and ongoing agency expenses.

Block out time each month to review and chart your standing expenses. This exercise will give you an exact picture of where your money is going, and areas you can cut back, and it’s particularly helpful if you’re feeling like the total costs of your business are more than you expected.

Remember to include MLS and association membership fees, real estate marketing and advertising spend, and incidentals like transportation.

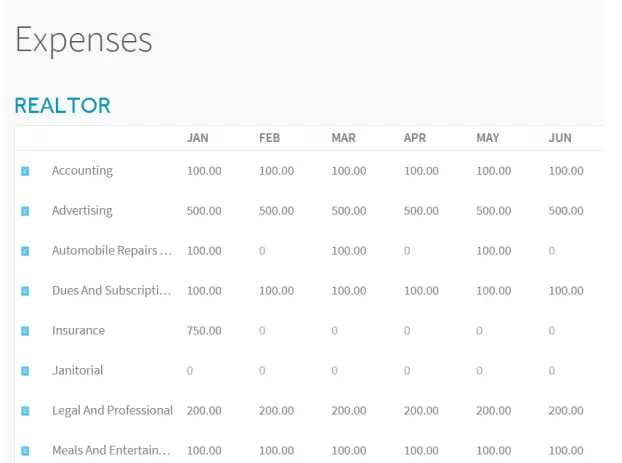

In the expenses example below from ProjectionHub, business necessities are accounted for by month. Creating a spreadsheet or chart and plugging in your business’s figures will give you a better overall picture of your finances.

- Plan for the inevitable slower months (“winter” is always coming).

- When you’re at the mercy of the unpredictability of the housing market (or simply working in the typical slow periods; usually the colder months — if you’re in a market that has cold months, at least), you absolutely need to be prepared for times when you likely won’t be seeing as much activity, by stocking and maintaining an emergency fund and keeping unnecessary expenses low. As much as we’d all love for consistent real estate success and income, anticipating the worst can make those times less troubling when they do happen.

- Consistently track your income and note major fluctuations.

- Maybe you were lucky enough to receive a hefty commission one month, but you scrambled to engage even one real estate lead 6 months later. Sock away unexpected extra income when you have it, and be aware of the actions you took that led to prospect to client conversions and the resulting sales.

- Allocate a considerable amount of funds for team growth.

- If down the road you plan to add employees to your team who will be paid a salary, like those who handle purely administrative or marketing tasks for you, be sure to earmark a portion of incoming funds toward their income.

Getting familiar with the particulars of your expenses and income is essential if you want to see substantial growth in your business, and in turn, have the ability to reach a broader range of prospects.

It’s no easy feat, but if you prioritize consistent monitoring of your revenue and your business goals, you’ll be on the right track to achieve them.

Learn the 80/20 formula that can help you become an even more successful real estate agent in this exclusive Placester webinar with KW’s Jesse Garcia:

What are your secrets to financial success as an agent? Share your business philosophy with us below!